Executive risk summary (early-2026 shift)

- In late 2025, the government signaled it would regulate meth contamination under the Residential Tenancies Act.

- Many insurance policies will automatically stop responding to meth contamination below 15 micrograms per 100 cm² when the regulation changes

- This could turn thousands of currently insured losses into uninsured events overnight

- Testing before the change may be the last chance to transfer this mid-range meth risk to insurers

Introduction

If you own rental property in New Zealand, there’s a significant change coming in early 2026 that could fundamentally alter your risk exposure—and most landlords don’t even know about it. Or, if they do know about it, they have not fully appreciated the implications this has for the costs they will bear for managing meth risk.

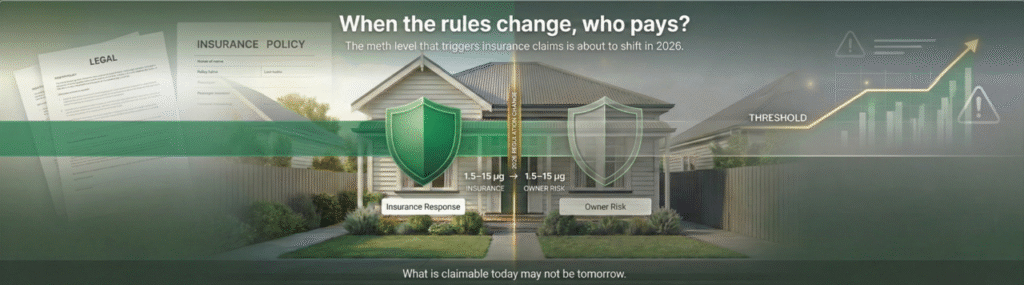

The government is proposing to regulate the acceptable meth contamination level for rental properties. This will change the statutory reference level from 1.5 micrograms per 100 cm² recommended in the NZ Standard to 15 micrograms per 100 cm². While this might sound like a technical adjustment, the implications for your insurance cover are substantial.

Understanding the Current Landscape

Insurance policies vary significantly in how they respond to meth contamination claims. The key lies in the policy wording—specifically, what contamination level triggers a claim response.

Following the release of the Gluckman Report in 2018, the market diverged. Some insurers adopted the threshold included in the report of 15 micrograms per 100 cm², while others aligned their policies with the NZ Standard or regulatory level of 1.5 micrograms per 100 cm².

This means two landlords with different insurers could have vastly different cover for the same contamination event. A property testing at 5 micrograms per 100 cm² might trigger a full claim response under one policy, while another policy wouldn’t respond at all.

The critical question for every landlord: What does your policy actually say?

Some policies specify a fixed contamination threshold. Others reference “the regulated level” or “NZ Standard” without stating a specific number. This distinction matters enormously for what happens next.

What Changes in 2026?

When the regulation shifts to 15 micrograms per 100 cm², policies that reference “the regulated level” or “NZ Standard” is expected to automatically adjust their response threshold—without any change to the policy wording itself.

This means contamination levels between 1.5 and 15 micrograms per 100 cm² that would trigger a claim response today may no longer be covered after the regulatory change takes effect.

Most insurers do not manually rewrite policy wordings when regulations change. Where a policy references “the regulated level” or “the NZ Standard”, that external benchmark becomes the moving part. When government shifts that benchmark from 1.5 to 15, the insurer’s exposure shifts with it automatically — without renegotiation, notification, or premium change.

If your policy specifies a fixed threshold (such as 1.5 micrograms), it may continue to respond at that level regardless of regulatory changes—but you need to check your specific wording to be certain and it should be considered likely that these policy wordings will change the next time they are renewed.

| Meth contamination level | Today | After the regulation change |

| 0 – 1.5 µg/100 cm² | Uninsured | Uninsured |

| 1.5 – 15 µg/100 cm² | Often insured | Often NOT insured |

| 15+ µg/100 cm² | Insured | Insured |

Why This Matters More Than You Think

You might be thinking: “If the government says 15 is ‘safe’, why should I worry about lower levels?”

Here’s the reality most landlords aren’t considering:

1. Real world research confirming the ‘safe’ levels the government is proposing has yet to be completed

Despite recommendations in the 2018 Gluckman Report to complete research and limited real world research (see here) suggesting a causal relationship between low level meth contamination and adverse health responses in some people, no additional research has been commissioned by government to confirm the assumptions that inform their policy.

2. Buyer and tenant expectations haven’t changed

Regardless of what regulations say, most property buyers and tenants want no meth in a property they’re purchasing or renting.

Pre-purchase meth testing is on the rise and any detection—even below the New Zealand Standard level let alone the new threshold—can affect salability and price.

We are likely to see a two-tier rental and housing market emerge: properties with documented meth clearance — and properties without. Banks, insurers, buyers, and property managers will increasingly differentiate between the two.

This is being driven by both the increase in meth use (see here) and the growing evidence that this use is contaminating housing stock (see here), which is now influencing how properties are valued, insured, and transacted.

Legal liability created by the new regulation also increases the risk for landlords who choose to ignore meth-related behaviour and contamination indicators.

3. The disclosure dilemma

If you know your property has contamination between 1.5 and 15 micrograms, you may face disclosure obligations when selling. A result that sits in this range could deter buyers or require price negotiation, even if it’s technically “compliant.”

Disclosure obligations when renting are yet to be determined.

4. The insurance gap

This is a key impact for those with policy responses linked to the NZ Standard.

After the regulatory change, contamination in the 1.5–15 microgram range becomes your problem alone for many policies. No insurance response. No claim. Just an out-of-pocket cost if you choose to remediate—or a potential sale impediment if you don’t.

5. Meth contamination of property set to continue to increase

Since the change of policy at the government level signalled by the 2018 Gluckman Meth Report, the levels of meth contamination have increased.

From a risk-management perspective, raising the threshold reduces the incentive for early detection and remediation — which historically has been the primary mechanism limiting long-term contamination of rental housing stock.

The Window of Opportunity

Right now, if your policy responds at the current regulatory level of 1.5 micrograms per 100 cm², you have a window where lower-level contamination will still trigger an insurance response. This window closes when the new regulations take effect in early 2026.

This is effectively a temporary opportunity to continue to transfer meth risk from your balance sheet to your insurer: test your property now, while you may still have insurance cover for lower-level contamination.

If testing reveals contamination above 1.5 micrograms:

- You may be able to make a claim under your current policy (subject to your policy terms and conditions)

- Remediation can potentially be completed with insurance support of all areas that exceed this reference level

- You’ll have documentation showing the property has been tested and cleared

- You eliminate a future sale impediment

If testing shows no contamination or levels below 1.5 micrograms:

- You have peace of mind and a baseline record

- You’re positioned to demonstrate a clean property to future buyers

- You can implement monitoring strategies going forward

What You Should Do Now

Step 1: Check your policy wording

This is the essential first step. Review your insurance policy carefully, looking for how meth contamination claims are triggered. Key questions to answer:

- Does your policy specify a fixed contamination level (e.g., “1.5 micrograms per 100 cm²”)?

- Does it reference “the regulated level,” “NZ Standard,” or similar language that ties to external benchmarks?

- What exclusions or conditions apply to contamination claims?

If you’re unsure, contact your insurer or broker for clarification. Don’t assume—confirm in writing if possible.

Step 2: Arrange testing

Commission a meth test from a qualified testing provider. This is a relatively low-cost investment that could save you significant money and stress.

Timing of the test for ongoing tenancies is an important consideration to discuss with your chosen service provider.

Step 3: Act on results

If contamination is detected above your policy’s trigger level, work with your insurer to understand your claim options. If levels are low or undetected, document the results and consider periodic retesting as part of your property meth risk management approach.

Step 4: Consider your tenant screening

Regardless of test results, review your tenant vetting processes. Prevention remains the best strategy and this is a key step.

If you are regularly testing make sure prospective tenants are informed this is being done. The value of a meth screening test is not finding meth, it is deterring the tenants with meth habits who will otherwise rent your home, but for the fact you can identify their behaviour.

The Bottom Line

The upcoming regulatory change doesn’t make meth contamination less of a problem for landlords—it simply shifts more of the risk onto the shoulders for many more policy holders. Properties with contamination between 1.5 and 15 micrograms may move from “insured loss” to “uninsured loss” overnight, depending on how your policy is worded.

Testing now, while insurance coverage may still apply to lower contamination levels, is a prudent risk management decision. It’s not about fear—it’s about understanding where you stand and taking action while you still have options.

Don’t wait until the rules change to discover a problem you could have addressed today.

Disclaimer: This article provides general information only and should not be taken as legal or insurance advice. Please consult your insurer and legal advisors for advice specific to your situation.